![]()

by Jorge Yui

Executive Summary

Ignoring the power of online word-of-mouth, or word-of-mouse as I like to call it, is no longer an option in today’s interconnected world. Nor is it reflective of what professionals in the financial services industry are being asked to deliver by their C-Suites post 2008. The ability of consumers to influence corporate behavior and impact business planning in unanticipated and, at times, unwelcome ways has grown exponentially. One ‘entertaining’ complaint from an irate customer going viral can escalate into a full-blown crisis in less than 24 hours. In this environment, understanding what customers feel, think and say about your company – in real time – is ever more critical.

Social Media: Two Sides of a Coin

Many corporations have discovered social media offers a new way of creating value and mutual benefit for the companies and customers. Take the case of Groupon who offer product vouchers to their customers in return for these individuals sharing their product experiences to their social networks. By engaging customers directly and incentivising them to sell the product, Groupon demonstrates a new way of selling that exploits the values inherent in social media networks. In the financial services sector, many retail banks use Facebook, Twitter, LinkedIn, Flickr and mobile applications, as well as social media tools on their own websites. In fact, Deutsche Bank, Crédit Agricole, BNP Paribas and Crédit Suisse employ a strategic approach[1} led by an in-house communications team.

40% of the banks use some type of social media (e.g. blogs, podcast or video casts, social bookmarking etc.) on their own website.

My Private Banking, Nov. 2010

Today, many companies seek to invest in their future by realizing the potential of social media. Where there is opportunity, however, often the other side of the coin is present as well: risk. And, in today’s world, the latter requires attention. In fact, according to the Economist Intelligence Unit[2], one of the most significant and delicate tasks facing corporations (added) in the 21st century is protecting their reputation.

Consumer-facing companies are rightly sensitive to brand stewardship and aware of how easy it is for an organization’s reputation, and its brand, to become tarnished or negatively associated with a larger, industry-wide issue. Today, consumer generated media is rapidly becoming the “voice of the people” with an ability to impact corporations’ bottom lines more significantly than ever before. In a survey of attitudes to blogs, 77% of respondents cited regularly updated journals as a useful way of gaining insights into the products and services they might buy.”[3]

With information available at the speed of thought, getting out in front of potential issues before it’s too late for anything but damage control is crucial. One needn’t look very far to find examples: A computer manufacturer and exploding laptops (Dell), a food manufacturer whose staff are filmed including rather disgusting things in their products (Domino’s), the uproar over the receptivity of the first iPhone in Twitter (Apple) or airlines/companies (Ryannair and United) who respond to unhappy customers by trading insults and fan the flames of a negative story. Each of these started in the social media sphere.

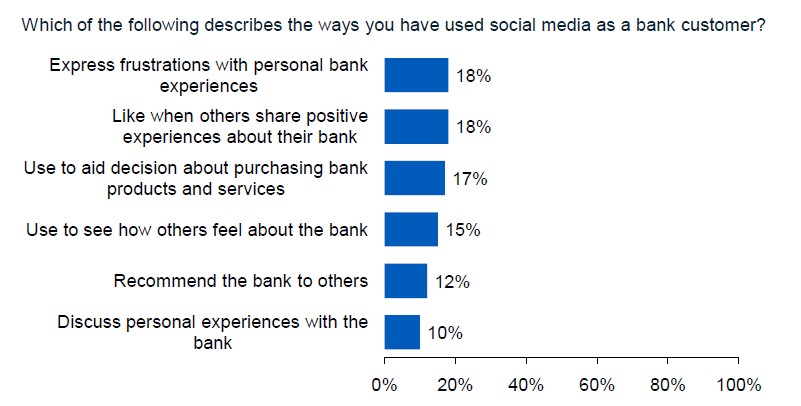

Many of us share ideas and opinions freely on blogs and Wikipedia or by leaving a comment on innumerable websites in ways we couldn’t have imagined just a few years ago. Reputation management in the financial services industry already faced significant challenges as a result of the growth of social media but the risks have been amplified by the 2008 banking crisis. In the US and the UK, trust in banks dropped 39% and 20% respectively between 2007 and 2010[4]. In fact, a survey of social media usage by bank customers (Figure 1) demonstrates just how we use social media. Respondents report posting both negative and positive comments, as well as reading the views of others. The reality is it is simply no longer possible to ignore this phenomena and I would suggest, means proactivity is the prudent business choice.

Figure 1 – Bank customers in social media[5]

Risk Monitoring: The Effect of Word-of-Mouse on Reputation

Today, many of us identify the brands we want to do business with by looking to our peers. In other words, if my friends trust or, even better, recommend a company, I will as well.

There are 500 million users on Facebook with 130 friends for an average user. According to the statistics, people spend 700 billion minutes per month on Facebook.

Facebook Statistics, May, 2011.

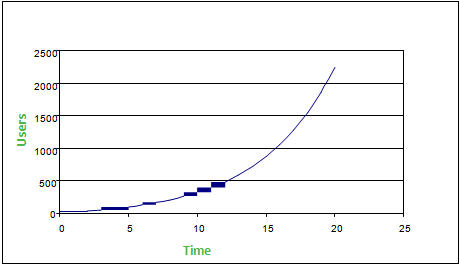

Viral coefficient is the number of new users acquired for each of the existing users passing through the viral loop. It is used to measure popularity in social media.

Figure 2 – Viral growth when viral coefficient is 1.2

70% of all blog and board postings are spam.

Institutional knowledge is the collective knowledge held within a corporation about brands, issues, talent, competitors and so on. When cross-referenced with key words, opportunities and risks are illuminated as they appear in the blogosphere, on message boards or other social media outlets.

But what about the issues you cannot identify? Institutional knowledge is essential but, by definition, it is gained through experience. The reality is, if you are unaware of an issue, you simply cannot track it. Using system knowledge, one can analyze trends immediately enabling the identification of significant events in real time.

Conclusion

Many sectors recognize the potential value of engaging with social media. The ever-growing influence of social media on consumer behavior presents companies with opportunities and risks while the massive amount of content enables the identification of previously unknown patterns, preferences and trends. To put it simply, using social media analytics to inform business strategy is just good business. Sorting the wheat from the chaff, however, is no small task.

___________________________________________________________________________

Authors

Jorge Yui is a senior managing consultant in the Strategy and Transformation Practice with IBM Global Business Services. He has participated in transformation projects in the Banking Industry in 17 Countries and in 4 Continents for over 20 years before joining IBM, where he now supports cross industry Clients in Geneva, Switzerland. Jorge can be reached at jorge.yui@ch.ibm.com

Key Contributors

Deniz Gunaydin – Consulting Intern, Financial Services Sector, IBM Global Business Services

Research Methodology

This paper uses our experience gained in client work at IBM, combined with secondary market research conducted in May 2011. We reviewed published articles, reports and papers to build up a picture of the opinion of subject matter experts from academia, business and industry analysts.

Examples of these information sources include Crédit Suisse Research Institute; TowerGroup; Facebook Statistics; Viral Loop by Adam L. Penenberg; The Wealth of Networks by Yochai Benkler; Wikinomics by Don Tapscott & Anthony D. Williams; Banking 2.0 by Brett King; GigaOM; Thomson Reuters; Finextra; My Private Banking; IBM SPSS; IBM developerWorks; IBM Research; IBM Institute for Business Value.

[1] Wealth Management and Social Media, MyPrivateBanking 2010

[2] Reputation: Risk of Risks, The Economist Intelligence Unit ©2005

[3] BBC Report (http://www.cymfony.com/know_center_blog.asp)

[4] The Democratisation of Personal Finance, Tracey Keys and Thomas Malnight, www.globaltrends.com, 2010

[5] Financial Services Customer Experience Survey, 2010