![]()

Symbiotics company profile map. Source: Symbiotics.

March 2015

The World Bank estimates that half of the world’s adult population – more than 2.5 billion people – does not have an account at a formal financial institution. Thanks to the rapid development of technology, today any point of sale can act as a bank and many people have since gained access to credit and banking services. However, with over one billion people still living on less than US$ 1.25 a day the role of microfinance and impact investment has been growing in importance in the past ten years. With sustainability being an increasing imperative for businesses and investors, the potential to make a positive impact on social and economic development is set to fuel continued rapid growth in the microfinance sector. To understand the dynamics of this important financial sector, we met with Symbiotics, one of the largest microfinance investment institutions with operations worldwide, to see what has changed since they launched their microfinance activities ten years ago – and what they expect ahead.

Global Trends: Where did microfinance start?

The origins of microfinance really date back to the 19th century when credit unions and rural cooperatives emerged to provide sustainable financial services to local customer bases, for example Banque Raiffeisen in Switzerland. Microfinance though then became the province of the development agencies in the 20th century, driven by large institutions such as the UN. However, they needed help channeling these monies to local markets, particularly in low income, frontier markets.

The next big milestone came in the 1970s when Accion in Bolivia and later the Grameen Bank in Bangladesh evolved from being conduits for these development monies into microfinance-focused banks in their own right. The first microfinance commercial fund available to investors was launched in 1998 but it was really only in the 2000s that the microfinance market really started to explode.

The UN Year of Microcredit in 2005 raised awareness of the opportunities among investors, as did the awarding of the Nobel Prize to Grameen Bank founder Muhammed Yunus. Since then it has grown at a rate of around 20% per annum. The market even did well during and since the 2008 financial crisis as the need is always there, and there is a lack of confidence in traditional banks to meet it.

Global Trends: What did the microfinance market look like when Symbiotics started its activities ten years ago?

When we started in 2005 there were no real experts in the sector – investors lacked information on what people and institutions in frontier markets needed and did not have the expertise to assess the credit risks involved. We came at the right time and were seen as pioneers in the field. Our founders came from Blue Orchard Finance, which was the first and largest microfinance fund. However, as an asset manager they had the challenge of being unable to serve some investors due to conflict of interest.

Symbiotics’ founders had a vision of creating positive impact and access to capital that would contribute to economic development in underserved economies. The business model overcame the challenges of conflict of interest, by acting as a service provider instead of an asset manager. This meant that we could work with a lot of different investors, including development agencies, private investors and investment funds, allowing us to scale our expertise and reduce the total costs in making investments from 3-4% to 2% or less. Then in 2008, some customers asked us to take a more active role in managing funds as they lacked the expertise, so with these first management mandates the company became a full asset manager.

Global Trends: How is Symbiotics achieving growth? What makes the company unique comparing to the numerous players in the market today?

In terms of volume of transactions, the potential market we focus on – investments to micro-enterprises – is huge, but in value terms it is still relatively limited with a market size of around US$ 10 billion. However, we have more people wanting to make investments than we have the capacity to handle at the moment. Having the people on the ground with the specific knowledge of the markets is a huge asset and we have built trust and visibility around our expertise and track record.

Big banks don’t understand illiquid frontier markets that do not offer investment grade assets and don’t want to manage many small transactions, so part of our role has been to educate them along with other investors. More recently these have included a growing number of pension finds who are starting to invest in microfinance although their legal obligations require that they emphasize returns ahead of social impact. Again this means that education of investors is important in terms of understanding both returns – which are not big generally in microfinance – and risks, as well as the potential for impact.

Combining these three factors into an effective investment approach is very complicated. Our approach is always to work through local financial institutions as this lowers risks to the extent that we can propose investments to mainstream investors. This means that while Symbiotics is one of the largest players in the world in terms of the market we focus on – originating around US$400 million annually in transactions, serving over 50 countries and 150 institutions – it can be tough to scale up, as we need to build expertise on the ground and relationships with local institutions. We are currently upscaling to an extent, moving towards targeting small as well as micro-enterprises, which means larger transaction sizes.

Global Trends: How do regional opportunities differ?

Microfinance, like many other activities, is impacted by global and regional trends such as political and economic crises. For example, Eastern Europe is less of a focus for microfinance today as pressure from a liquidity crisis combined with the post-Balkan crisis means the region has received substantial amounts of development aid from the EU. In Central Asia, the Caucasus regions do use microfinance but are seeing the impact of the Russian/Ukrainian political crisis.

From our perspective, the fastest growing region is Africa where we have recently received mandates from development agencies worth US$ 150 million to develop microfinance in Sub-Saharan Africa. We also cover 12 markets in Latin America and the Caribbean, which is historically a strong region, and seven in South East Asia. However, there are geographic differences in the issues faced. In Africa the issue of reaching the unbanked is distance and infrastructure is poor, so technology is the main solution. In Latin America the challenge is building credibility of the local institutions and moving people away from dependence on an aid culture. Asia has not historically been a major focus although we have some activities in Cambodia, Indonesia and the Philippines. Looking forward, the next bog market in Asia is likely to be India and with the microfinance system being rebuilt, the conditions are becoming right to invest.

Global Trends: What are the biggest challenges Symbiotics and microfinance face today?

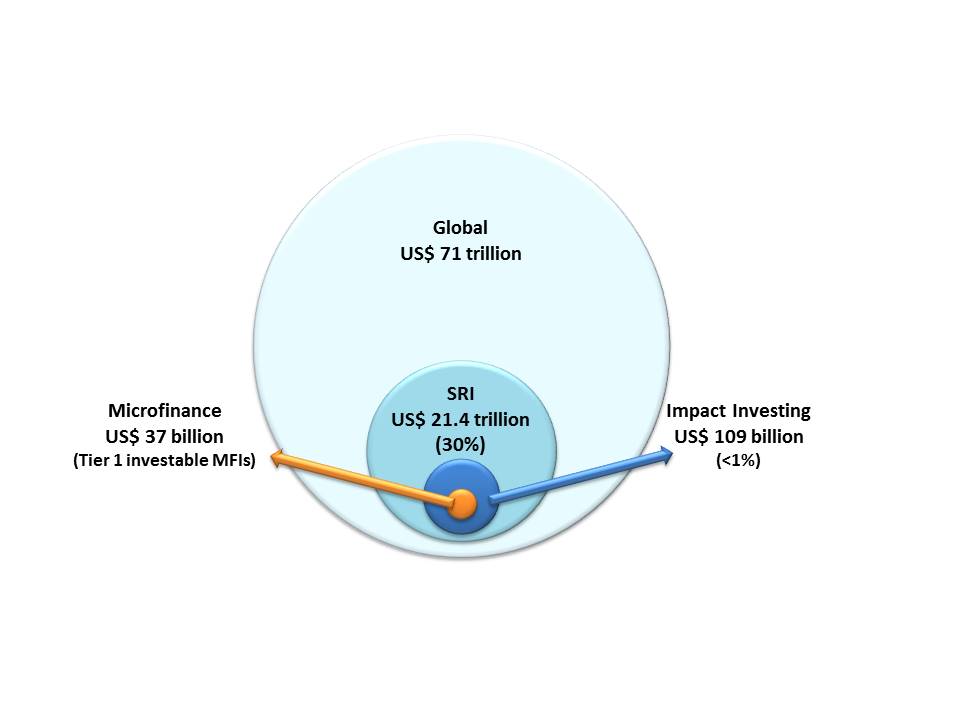

One of the biggest challenges is helping investors to understand the different definitions of impact investing, socially responsible investing and the different types of microfinance, as there is a lot of confusion around the terms. Socially responsible investing is a sub-set of overall investing which is estimated to be around US$ 21.4 trillion, and the philosophy of this sector can be characterized as “do no harm.” Within this “pie” There is a smaller sub-set we call impact investing, which moves from not doing harm towards a philosophy of actively “doing.” And an even smaller sub-set within impact investing can be termed microfinance as this is where the focus is doing good working with the smallest borrowers and enterprises.

Our focus is specifically on investments in micro-enterprises and some smaller enterprises, so our sector is within the smallest sub-set in the chart below. This is very different from what could be termed “consumption finance” where, for example, companies offer credit cards in Mexico to finance consumption or lease finance. There is an increasing level of competition in the microfinance market from such companies, but the models are generally not sustainable.

Sources: Global sustainable investment review 2014, Bloomberg, http://www.gsi-alliance.org/wp-content/uploads/2015/02/GSIA_Review_download.pdf; responsibility Microfinance Market Outlook 2014, http://www.responsability.com/funding/data/docs/en/1872/rA-Microfinance-Market-Outlook-2014.pdf.

Sources: Global sustainable investment review 2014, Bloomberg, http://www.gsi-alliance.org/wp-content/uploads/2015/02/GSIA_Review_download.pdf; responsibility Microfinance Market Outlook 2014, http://www.responsability.com/funding/data/docs/en/1872/rA-Microfinance-Market-Outlook-2014.pdf.

Another challenge is that people simply don’t understand what we do, so they may say “Why don’t we get a return of 20% for the high risk of investing in Kyrgyzstan?” This criticism does not reflect how we actually make investments: In a typical portfolio, there are investments in 30 to 40 countries, with financing being made available to small institutions and lenders, so national macro-economic risks have a limited effect. Therefore demanding returns that equate to country-level risks is not a good comparison.

There are also reputational risks with microfinance. High profile stories such as those in recent years of suicides in India by people who had received microfinance and were unable to manage their debts have taken a toll. However, the problem of microfinance in India reflects the issues of a lack of regulations to govern lending and political intrusion. The government there now is working hard to rebuild the system so we hope to see a more positive lending environment and impact in future. It is important though to manage these challenges through education – for example, we help journalists visit countries to see the realities on the ground, so that they can develop accurate stories.

Global Trends: Do you feel an impact from increasing competition and “big” players coming in?

Quantitative easing (QE) around the world has created a lot of liquidity in the financial system, with an increasing number of institutions and funds available to potential borrowers, so competition has increased. However, QE has also created many distortions, for example with competition to lend driving returns down, sometimes to a point where they become negative once inflation is considered.

In terms of the competitors themselves in microfinance, some of the big banks are going “down market,” starting to serve smaller customers to increase their customer base. Other banks and investors are actively trying to understand the market to see where it makes sense to invest, although they cannot always invest as much as they want because of the complexity and capacity of the channels. The number of investable institutions (Upper tier 2 and tier 1 in the chart below) in microfinance investment today is around 300 of a total of 10,000.

Another trend to note is that while the market is going 20% year on year, the percentage of international funding involved is going down. This is because many more local politicians are getting involved, applying local public funds to microfinance uses to help drive social and economic development.

Global Trends: Many new financial innovations are emerging from microfinance to virtual currencies, with new players that are not traditional financial institutions entering the market. With these changes there is increasing talk of new regulations and legislation. What do you see as the key areas that will see new regulation? What do you anticipate will be the impact for Symbiotics?

As an asset manager, we are already regulated, although obviously the regulatory environment differs by country. For microfinance, regulation has been a positive in helping develop and grow the sector, for example, in Bolivia where regulations were developed that were specifically adapted to the sector. Central banks are also now viewing microfinance as a “legitimate” banking sector, although non-financial players such as NGOs are typically not regulated except in Bolivia, and there are fewer regulations on the type of consumption-focused lending we discussed earlier.

Global Trends: Looking forward, how do you see microfinance developing?

We expect the microfinance market to continue to grow around 20% a year, as it has in the past decade. There are 175 million clients currently served by microfinance, but the potential market in demand is 2.5 billion.

One of the big areas of focus will be measuring the real impact of the financing on the ground. While we can already measure the outreach – number of people and micro-enterprises receiving loans, and average transaction size, for example – no-one has yet succeeded in quantifying the impact of this financing is having on social and economic indicators, such as increasing average incomes or contributing to long-term success of small businesses.

Source: Symbiotics, 2013.

Source: Symbiotics, 2013.

We have partnered with Oxfam in a project to look at these issues, and also work with the local financial institutions, but are not there yet. However, we do use samples of stories from borrowers to measure impact in a qualitative way.

Global Trends: What impact have technology advances had on your business and the sustainable investment sector more broadly? How do you use technology to get in touch with your investors?

One example could be the rise of mobile banking in Kenya. Mobile phones help in this region as they allow low income populations to access banking accounts despite the lack of infrastructure. At the same time we could ask ourselves the question: “There are lots of subscribers or registered users, but is anyone actually using it?”

We attract and contact our investors mainly through our website and our membership in larger associations such as the PRI, GIIN, and Sustainable Finance Geneva. We are not actively involved in social media as we seek very specific groups of people geographically and qualified investors. Many of our communication tools and publications are rather for awareness purposes and to let the wider public understand more about the market, activities and terminology.

Global Trends: Looking ahead, what do you see as the most exciting opportunities for Symbiotics – and the challenges to address in the coming 5 and 10 years?

What motivates us the most is doubling our size over the next three years and reaching US$ 2 billion in our portfolio and 2 million low and middle income households and micro-, small and medium enterprises.

We want to achieve this aim by investing beyond microfinance into: Agriculture, energy, small and medium enterprises and housing. We also want to be more active in equity markets and technical Assistance.

CEO Roland Dominicé says: “We’re very happy about this next phase of our development into new markets in the wider impact investing universe.”

What motivates us is making our current and future projects a success and achieving continued growth. If we can offer those 2.5 billion people and businesses sustainable, credible products that would personally be very exciting.

There are clearly opportunities to go beyond the microfinance and even SME sectors, but the challenge will be deciding where and how. In terms of the where, there is the potential to develop investments in specific themes such as education and housing, where we can also offer local institutions technology assistance. Other sectors such as energy and health would likely require partners.

In terms of how, there are opportunities to expand our bond platform and it would be exciting to develop these into mainstream financial instruments that we can promote the use of in capital markets.

In ten years, for us as a company though, the key will be success in keeping our values and culture. Success is about the way we do things as well as success in the microfinance sector – we started as a group of young, enthusiastic people full of energy to travel and make a difference. 25% of employees are shareholders which gives us a real stake, and we have an independent board. While we currently need to do some integrating and consolidating because we have grown so fast in recent years, the culture is critical – and brings a lot of people back to the company even after they have left.

***

Defining microfinance investments: A brief glossary

Micro-credit refers too financing solutions offered to micro-enterprises, limited to lending instruments, as opposed to SME financing which refers to a wider array of financial solutions and concerns a greater span of enterprises, also bigger in size and usually formally registered. (Source: Symbiotics)

Microfinance is the provision of financial services to micro-enterprises and low income households, whether through credit, savings, insurance and/or payments/remittances. (Source: Symbiotics)

Microfinance institutions (MFIs) are financial intermediaries which are specialized and dedicated to micro-enterprises and low income households. (Source: Symbiotics)

Impact investing is defined as investments made into companies, organizations and funds with the intention of generating measurable social and environmental impact alongside a financial return. (Source: As defined by the Global Impact Investing Network, GIIN)

Whereas Socially responsible Investing fund managers are generally passive and apply a “do no harm” approach, impact investing funds typically seek to create positive impact and measure and report the impact in a transparent way. (Sources: TriLink Global, Symbiotics)

Sustainable finance refers to any form of financial service integrating environmental, social and governance (ESG) criteria into the business or investment decisions for the lasting benefit of both clients and society at large. (Source: Swiss Sustainable Finance)

Source: A Guide to Responsible Investing, Microrate 2013

Facts and figures on Symbiotics

· Founded in 2005

· 85 staff in 6 offices

· US$ 2 billion originated, US$ 1 billion under management

· Over 200 MFIs in around 50 countries

· Working with more than 28 investment funds

Symbiotics is an investment company specialized in emerging, sustainable and inclusive finance which offers market research, investment advisory and asset management services. It is a regulated asset manager of collective investment schemes by FINMA, the Swiss Financial Market Supervisory Authority and has an advisory license from the FCA, the Financial Conduct Authority in the UK. The company is headquartered in Geneva, with offices in London, Mexico City, Singapore and Cape Town. The company also offers Syminvest, a microfinance investment intelligence platform designed to increase transparency and enhance investment capacity in the industry by monitoring regional markets as well as individual institutions. From 2004 through July 2014, Symbiotics provided USD 811 million in capital to 803,000 micro-, small and medium-sized enterprises (MSMEs) through 150 financial institutions.

(Source: Symbiotics)